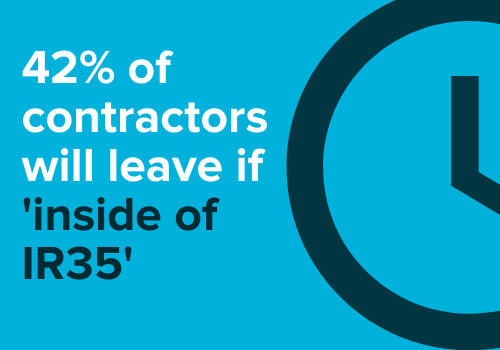

In the most recent Salt survey, 42% of our respondents expressed that they would leave their role if the end-client determined the assignment to be inside of IR35. Based on the results, Salt’s Head of Compliance & Contractor Management, David Korthals, and Sales Director, Richard Norris, provide insight into contractor’s perceptions of IR35 and how Salt’s clients are managing the legislation changes.

But before we jump into the results of our survey, let’s look at what will change…

As you’re most likely aware by now, changes to the IR35 tax legislation are due to roll out in April 2020. However, the legislation is still awaiting approval from the UK Government.

What is IR35 in the private sector going to look like once approved?

IR35 is the name given to tax legislation in the Income Tax (Earnings and Pensions) Act 2003. It was originally introduced in 1999 to deal with alleged tax avoidance via the use of Personal Service Companies (PSC’s).

Currently, your PSC needs to declare whether you work inside or outside IR35. HMRC has claimed that only 10% of all PSC’s apply the current IR35 rules (and thus account for PAYE) and have estimated the costs of alleged non-compliance to reach £1.3bn in 2023-24.

The most important change under the proposed legislation will be that the end-user (in the staffing industry also known as the hirer or end-client), and not the contractor PSC, is required to determine the contractor’s tax status. Our previous post highlights the details of the new legislation.

How have end-users responded so far?

Regrettably, some companies (especially major financial institutions) seem to have taken a blanket approach. They have either decided that the current assignments need to be classified as ‘inside IR35’ or they have applied a hiring model under which recruitment businesses are simply not entitled to engage with limited company contractors. Moreover, many other end-clients are still not able to confirm when the IR35 determinations will be made.

We have already received calls from contractors who are not willing to extend the assignment beyond the end of January 2020 if no specific, tailored determination is made about their role status.

So how do contractors feel about the changes?

In September 2019, we carried out a survey and asked contractors how they were feeling about the changes. Here are some of the results:

- Some contractors commented that they already predicted the flexible workforce will be removed completely for short-term projects

- 22% of our contractors already had a conversation with their client regarding IR35

- However, 45% of those did not believe their status would be determined adequately

Taking this and our most recent survey into consideration, it is paramount for end-users to act now if they want to maintain a (compliant) contractor workforce. The results below reflect this:

- 42% indicated they would leave the role if the assignment is deemed to be inside IR35

- 31% will challenge the decision if their role is determined to be inside IR35

- 59% of our respondents have not received a status determination yet and only 34% have received a confirmation that an assessment will be made soon

- 38% of our contractors already want to speak about their expected IR35 status

It is obvious that clients need to ensure that contractors receive a proper determination (that considers the specific details of each assignment) in order to attract and retain the best talent.

Salt is not advocating a blanket approach whether this is inside or an outside IR35 determination (the latter can be regarded as tax evasion). However, by taking a blanket approach or simply enforcing contractors to work PAYE, they face potential disruption to their contingent workforce due to contractors leaving the assignment or time spent dealing with those contractors challenging the decision.

Moreover, by not taking the appropriate time and effort to make a proper and accurate determination based on the role and engagement model of the contractor, end-clients may face increased exposure to fines imposed by HMRC.

There is no need for this if all parties in the chain work together.

How can we help our clients and contractors?

Salt’s IR35 project group was set up to help both candidates and clients navigate their way through this somewhat ambiguous piece of legislation.

We have invested in a case-based, insurance-backed assessment tool which will make quick and accurate assessments and manage the communication and recording of the determinations to ensure a compliant supply chain.

For more information about our IR35 services, visit our webpage or get in touch with the team today.

What we provide:

• IR35 awareness workshops

• IR35 assessment tool

• Supplier & Contractor Review

• Contractor Management Platform

Additionally, we provide our contractors with up-to-date guidance on how we manage the legislation changes to create compliant futures for our clients that will positively impact the digital economy.

For more information or advice on digital hiring, get in touch with the team today at contact@welovesalt.com.